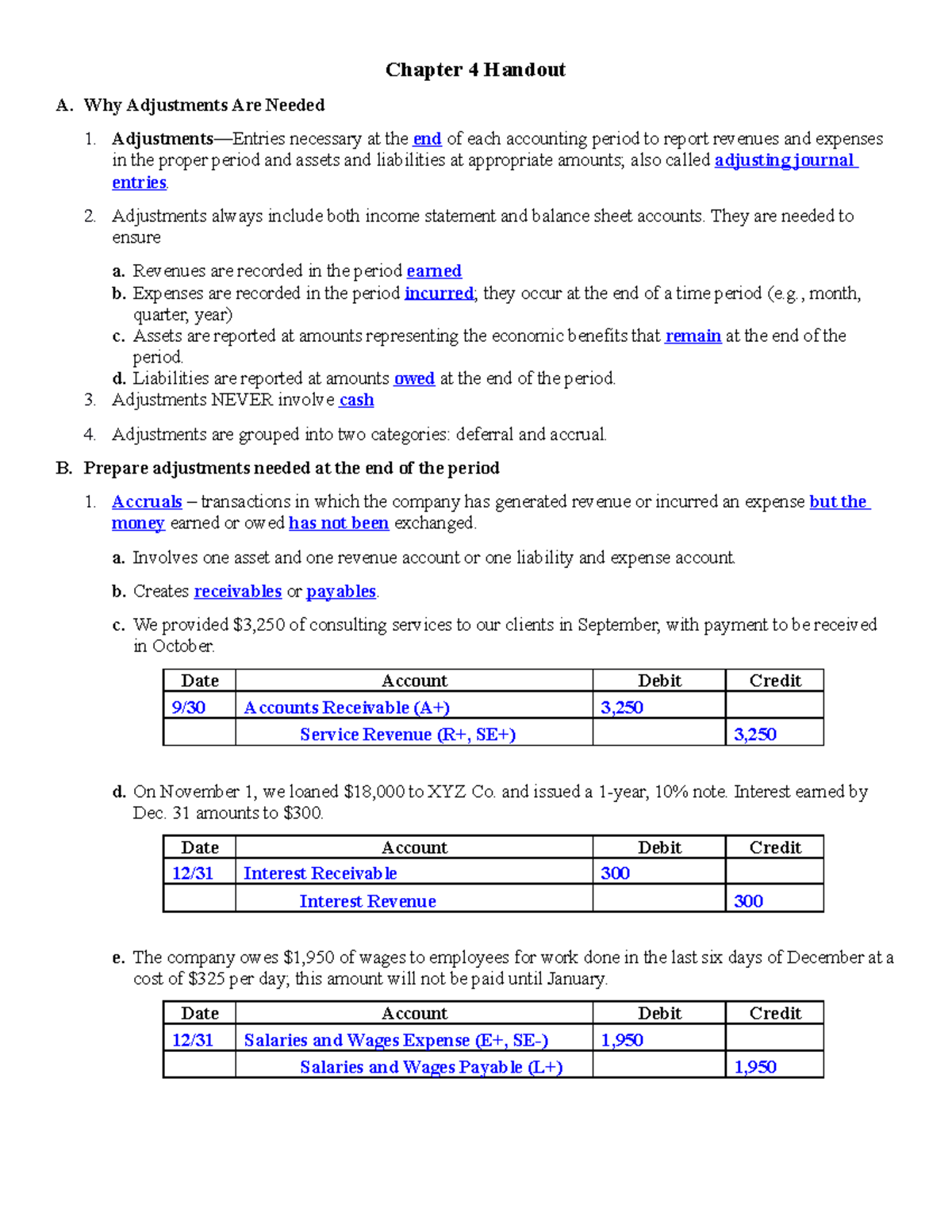

Your revenue enhanced

Done well! You got an advertisement otherwise become another type of employment, that has increased what kind of cash obtain on your own wages. This will be a captivating time, so using a mortgage calculator to see the best way to shorten the phrase of borrowing may come with swells regarding delight. Hand calculators will show that plumping up your repayments by the actually an effective small amount will cut months otherwise decades from the name out-of your loan. Highest repayments imply shorter attention plus dominating every time you create a home loan repayment.

Team supposed gangbusters

Jake and Tom is one another lives and you can company lovers, in addition to their company was roaring. In two age, their earnings has doubled and there are contracts getting toward upcoming. Jake and you can Tom own a property together, which they purchased five years back. In those days, they might hardly scratch a deposit to each other, so that they selected a 30-12 months home loan label to save money reduced. They are going to correspond with the current bank, and two various other financial institutions. As the entrepreneurs, Jake and you will Tom is actually experienced; they are going to drive a difficult contract and choose the clear answer that’s extremely beneficial.

You’ve got a windfall

Perhaps a close relative bequeathed your a clean amount of cash. Or if you marketed a business, assets or a greatly rewarding line of artwork/stamps/bitcoin. Or it may be you received an advantage otherwise had lucky’ at the Lotto. No matter what cause, a windfall is usually to be recognized and you may made use of intelligently. Settling an amount of your own mortgage is obviously good tip. You’ve got the option of breaking of with your bank otherwise which have a talk with your current lender (make sure you ask about any split fees or split will cost you). Brand new lump sum commonly reduce the term of one’s mortgage, so you will be obligations-totally free ultimately.

Individuals would like to show the debt

Perchance you located the permanently spouse, had a sister/mother move around in with you otherwise want to split property having a friend. Long lasting story, an individual otherwise wants to donate to the mortgage, and also you consider it is best, you will be in a position to enhance your repayments. Their financial pal can even possess a lump sum to take down their loan’s prominent. With this particular change in circumstances, you might refinance their home loan or restructure so you can a combined home loan. Its a time for you shop around to have another bank and you can issue the financial https://paydayloancolorado.net/upper-witter-gulch/ to part of which have a good bring.

Flatmates end up being life lovers

When Harry moved towards Hazel’s household as a beneficial flatmate, they easily became close friends. And they truly became over members of the family. 2 years later on, Harry and Hazel decided to tie the knot economically, of the relocating to a contributed home loan. Fortunately, the newest fixed home loan to own Hazel’s family was only coming up to have restoration. Thirty day period until the rollover big date, Harry and you can Hazel talked on the existing bank about their economic problem and you can a unique loan. Their package would be to place the family with the both the labels, pay a lump sum payment of (Harry’s discounts) and you will shorten the mortgage label.

Costs associated with refinancing

While refinancing otherwise restructuring their home loan can save you currency, discover apt to be charges associated with process, particularly when you’re using a brand spanking new bank or bank.

- Break charge you have home financing contract in position along with your bank that will have seen your paying rates of interest into the loan inside the long run. So you’re able to re-finance, you happen to be breaking it arrangement to begin with another, which means your latest lender manages to lose one anticipate funds. The fresh Zealand laws means banks to incorporate a choice for repaired price agreements become busted, and in addition lets these to cost you to recover will cost you. To find out just what split fees otherwise split will set you back would-be inside for the problem, confer with your newest lender otherwise lender.